Market Update: April 27, 2026

U.S. equity markets paused last week following a strong April rally, with most major indices finishing flat and the S&P 500 still up nearly 12% from its late-March lows. The Nasdaq-100 stood out with a ~2% gain, driven less by mega-cap leadership and more by strength in semiconductors, supported by improved outlooks across the chip sector.

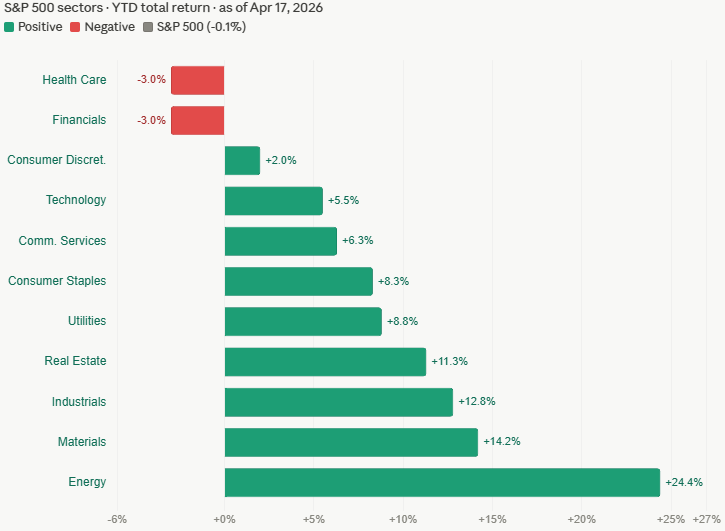

Macro conditions remain complex. Oil surged, with WTI nearing $95 per barrel amid continued geopolitical tension surrounding the Strait of Hormuz. While diplomatic developments briefly eased prices, energy markets continue to inject inflation risk into the outlook. Accordingly, Treasury yields drifted higher and expectations for near-term Fed rate cuts continued to fade.

Despite these headwinds, U.S. economic data points to resilience. March retail sales rose 1.7%, the strongest monthly gain in over a year, while PMIs remained in expansion territory. Housing activity also showed strength, with pending home sales rising despite elevated mortgage rates. However, consumer sentiment remains weak, highlighting a growing disconnect between “soft” and “hard” data.

Globally, conditions are less stable. European economic indicators continue to soften, while inflation pressures persist across the U.K., Japan, and Australia. Combined with a stronger U.S. dollar, this has weighed on developed international markets.

Looking ahead, markets are focused on the Fed, core PCE inflation, Q1 GDP, and a critical wave of mega-cap tech earnings. With equity valuations elevated and geopolitical risks unresolved, the sustainability of recent gains will likely depend on earnings delivery, energy price stability, and clarity from policymakers.

The information above has been obtained from sources considered reliable, but no representation is made as to its completeness, accuracy or timeliness. All information and opinions expressed are subject to change without notice. Information provided in this report is not intended to be, and should not be construed as, investment, legal or tax advice; and does not constitute an offer, or a solicitation of any offer, to buy or sell any security, investment or other product.