Market Update: July 6, 2026

For illustrative purposes only. The graphic depicts a general investment approach and is not intended as personalized investment advice. Asset allocation and model selection will vary based on each client's objectives, risk tolerance, financial circumstances, and investment time horizon.

Last week’s market narrative shifted quickly as a weaker-than-expected labor report altered the outlook for both Fed policy and equities.

June payrolls came in at just 57,000, and prior months were revised down by a combined 74,000. While the unemployment rate ticked slightly lower to 4.2%, slowing job creation and a drop in labor force participation to a five-year low point to a gradually cooling labor market.

Markets responded decisively. Rate hike expectations were repriced lower, with July odds falling to 15% and September to 60%, effectively removing one anticipated hike from the 2026 path. This shift helped stabilize equities following last month’s volatility spike.

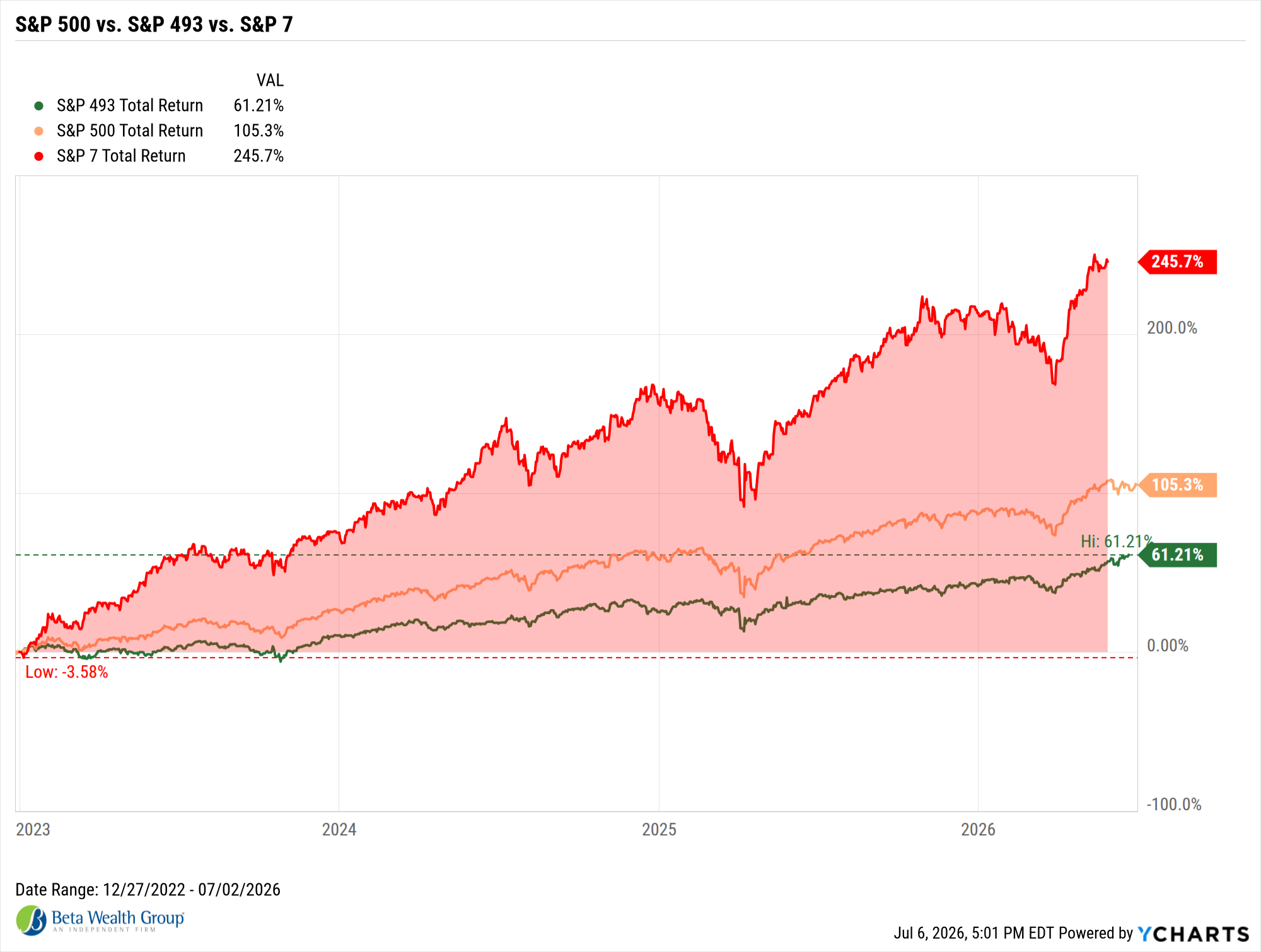

Risk assets rallied as a result. The VIX fell toward 16, near yearly lows, while mega-cap tech rose roughly 6% on the week. Cyclical sectors, including financials, communications, and consumer discretionary, outperformed, signaling renewed risk appetite. Meanwhile, defensive sectors lagged, and energy stocks weakened alongside oil prices.

However, uncertainty remains. New Fed Chair Kevin Warsh reaffirmed the 2% inflation target but stepped away from clear forward guidance, introducing a layer of ambiguity markets will need to adjust to. Treasury yields moved higher following his remarks, reflecting that tension.

Looking ahead, the focus shifts to confirmation: FOMC minutes, jobless claims, and PMI data will help determine whether last week’s labor data marks the beginning of a broader slowdown or a temporary soft patch.

For investors, the takeaway is clear: the market remains highly sensitive to incremental changes in growth and policy expectations, with leadership continuing to favor sectors tied to economic resilience and rate stability.

The information above has been obtained from sources considered reliable, but no representation is made as to its completeness, accuracy or timeliness. All information and opinions expressed are subject to change without notice. Information provided in this report is not intended to be, and should not be construed as, investment, legal or tax advice; and does not constitute an offer, or a solicitation of any offer, to buy or sell any security, investment or other product.