Market Update: February 24, 2026

U.S. markets continue to climb a wall of worry, balancing softer macro data against shifting policy and geopolitical risks.

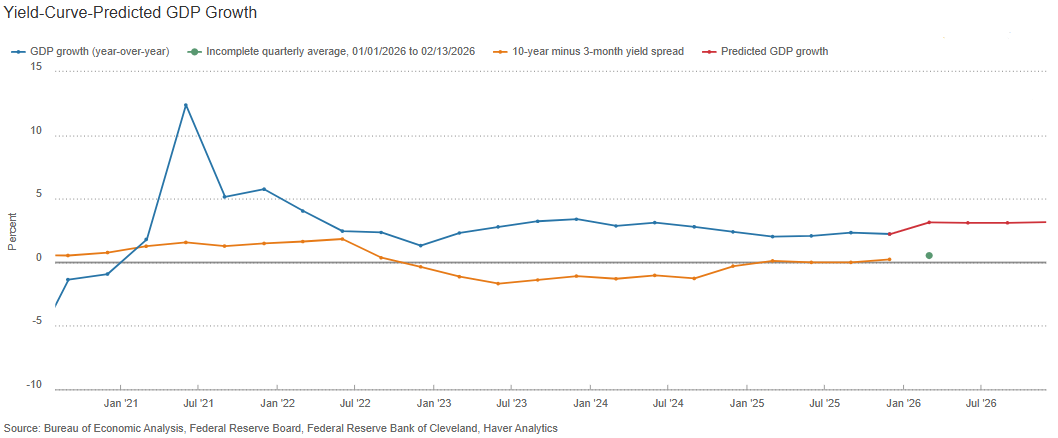

Last week, major U.S. equity indices advanced, led by the Nasdaq, with financials, communications, and industrials outperforming even as staples, materials, and healthcare lagged. In single-name news, Walmart traded lower on cautious guidance, while in commodities silver spiked sharply and gold firmed. Treasury yields moved higher as the first estimate of Q4 2025 GDP disappointed at 1.4% versus 4.4% in Q3, and Core PCE re-accelerated, keeping the Fed’s 2% inflation target very much in play.

The Supreme Court’s decision to strike down President Trump’s sweeping tariffs adds a new, complex policy variable. Key questions now include potential tariff refunds, timing, and how the U.S. might replace lost revenue amid already stretched public finances. For investors, this ruling has implications for globally exposed sectors, tariff‑sensitive industries, and the longer end of the yield curve as markets reassess the fiscal outlook.

Globally, the picture is mixed but improving at the margin. Business activity in Europe is surprising to the upside, with Germany’s manufacturing PMI finally back in expansion, while the U.K.’s softer inflation and labor data strengthen the case for earlier rate cuts. In Asia, weaker Chinese inflation underscores an uneven demand recovery and the likelihood of continued policy support.

In the week ahead, a lighter data calendar shifts the focus to:

Nvidia and Home Depot earnings and their guidance;

U.S. PPI, confidence, and factory orders;

Comments from Fed officials and fresh inflation prints from Germany, Japan, and Australia.

Volatility remains event‑driven, but for now, the cyclical backdrop and easing bias from central banks continue to underpin risk assets.

The information above has been obtained from sources considered reliable, but no representation is made as to its completeness, accuracy or timeliness. All information and opinions expressed are subject to change without notice. Information provided in this report is not intended to be, and should not be construed as, investment, legal or tax advice; and does not constitute an offer, or a solicitation of any offer, to buy or sell any security, investment or other product.