Market Update: July 13, 2026

For illustrative purposes only. The graphic depicts a general investment approach and is not intended as personalized investment advice. Asset allocation and model selection will vary based on each client's objectives, risk tolerance, financial circumstances, and investment time horizon.

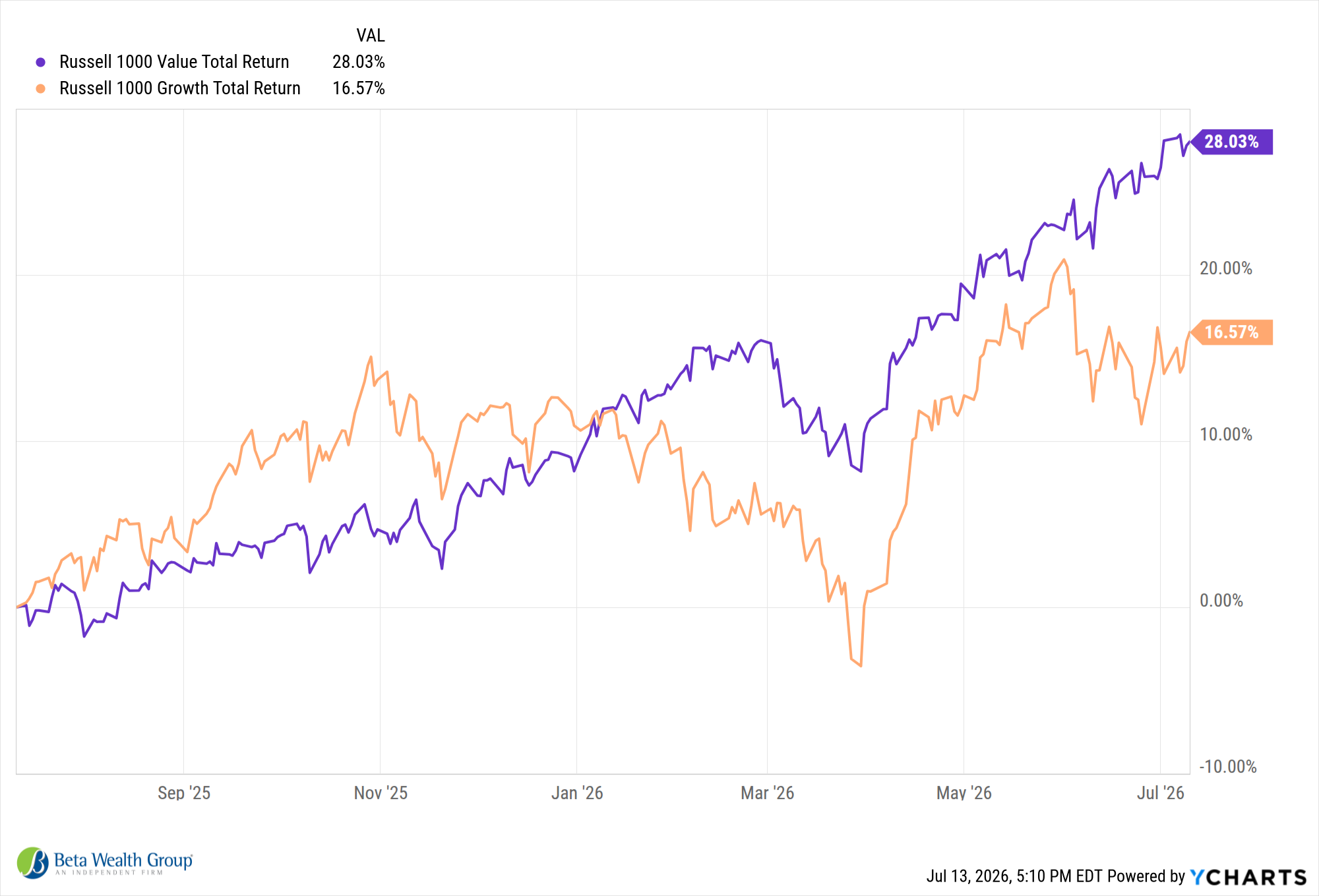

Last week’s market activity reflected a familiar dynamic: resilient economic data, rising geopolitical tensions, and continued debate around inflation’s path forward.

On the macro front, ISM services softened slightly but remained in expansion territory, while existing home sales declined. Meanwhile, FOMC minutes reinforced the Fed’s ongoing concern that inflation - particularly driven by energy prices and structural investment in AI - may prove more persistent than expected.

Markets responded with mixed performance. U.S. equities saw strength in technology and energy, each gaining over 3%, while materials, healthcare, and industrials lagged. Large caps outperformed small caps, and sector leadership continued to rotate. Beneath the surface, factor volatility remains notable. Momentum has been driven by semiconductors, while “quality” stocks have underperformed, challenging many traditional portfolio tilts.

Geopolitics re-emerged as a key driver. Escalating tensions in the Middle East, including renewed strikes impacting shipping routes, pushed crude oil prices higher and contributed to rising bond yields. The 10-year Treasury moved back above 4.5%, pressuring fixed income broadly and widening credit spreads.

The AI theme remains central. Despite early-week weakness in semiconductor stocks, strong investor demand for AI infrastructure was reaffirmed by SK Hynix’s record-setting U.S. IPO. This underscores continued capital commitment to the long-term buildout, even amid short-term volatility.

Globally, markets were mixed. Japan benefited from policy support, while Europe and parts of Asia lagged. Emerging markets saw pockets of strength, particularly in Brazil and China.

Looking ahead, focus shifts to Q2 earnings, inflation data (CPI/PPI), and Fed Chair commentary. With inflation, geopolitics, and AI all in play, expect continued cross-asset volatility & and opportunity for selective positioning.

The information above has been obtained from sources considered reliable, but no representation is made as to its completeness, accuracy or timeliness. All information and opinions expressed are subject to change without notice. Information provided in this report is not intended to be, and should not be construed as, investment, legal or tax advice; and does not constitute an offer, or a solicitation of any offer, to buy or sell any security, investment or other product.