Market Update: June 22, 2026

Markets navigated a holiday-shortened week with a mix of geopolitical developments, central bank decisions, and uneven economic data.

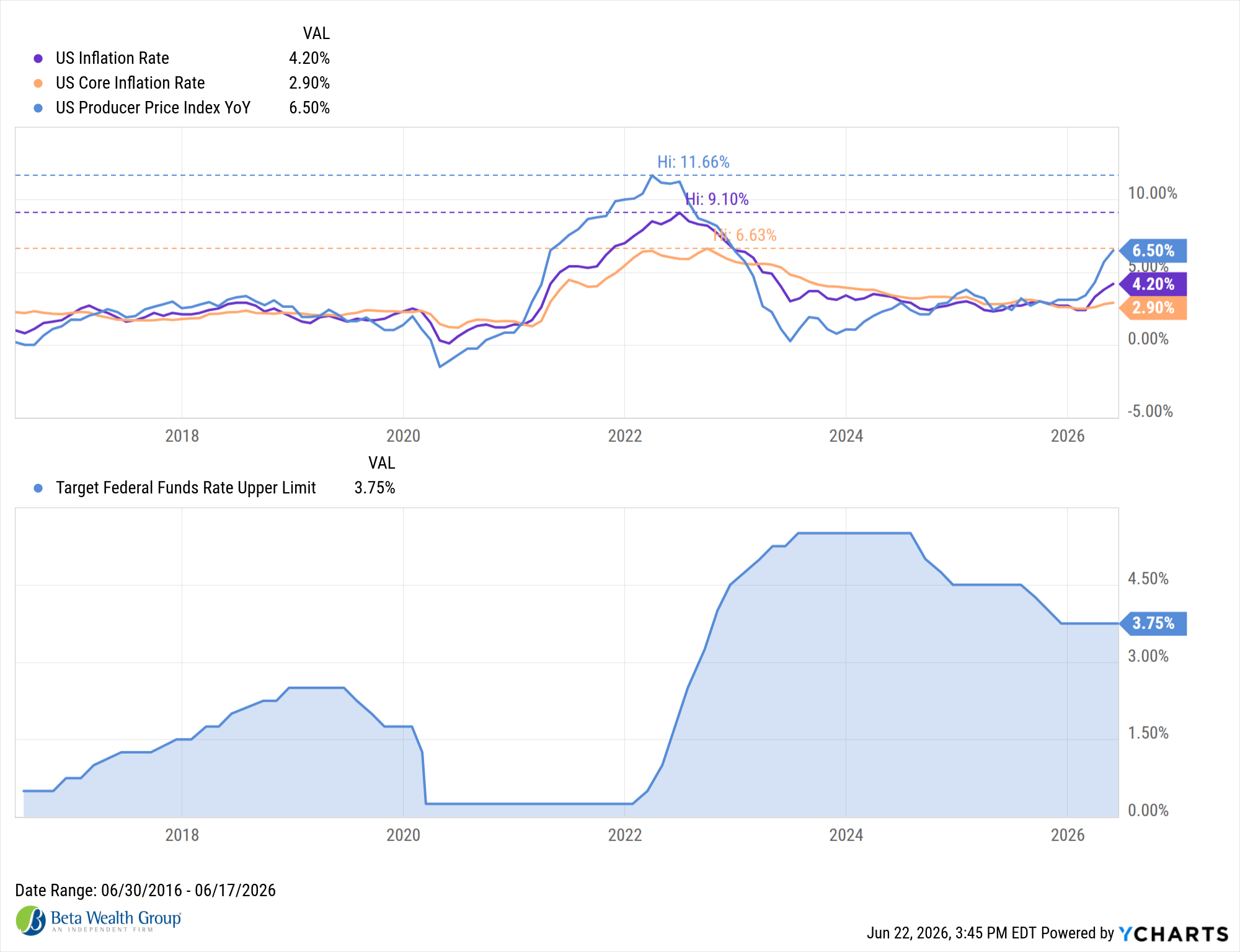

The Federal Reserve held rates steady, while retail sales and industrial production showed resilience. However, housing data softened, with declines in starts and homebuilder sentiment signaling continued pressure in interest-rate-sensitive areas.

The dominant market driver was geopolitics. A preliminary U.S.–Iran agreement, including plans to reopen the Strait of Hormuz, helped ease global risk concerns and pushed equities higher. U.S. stocks advanced, with leadership broadening beyond mega-cap tech. Industrials and technology both gained 3%, while equal-weight indices outperformed. Energy lagged, falling over 6% alongside a steep drop in oil prices, while defensive sectors also trailed as risk appetite improved.

Globally, equities followed suit. Asian markets benefited from reduced energy risk, while Europe advanced despite an ECB rate hike. Central bank divergence continued, with the Bank of Japan raising rates to 1.00%, a notable shift after decades of ultra-loose policy, while the Bank of England held steady.

Fixed income markets were relatively calm. Treasury yields moved modestly lower, and the curve remained flat, reflecting mixed signals between cooling inflation expectations and still-firm economic data.

Commodities told a clearer story. Oil prices dropped roughly 9–10% on the week as geopolitical tensions eased. This marks a significant reversal after extreme volatility earlier this year, with crude now materially off its April highs.

Overall, markets appear to be recalibrating: less driven by worst-case geopolitical scenarios, and more focused on growth durability, policy direction, and the path of inflation.

The information above has been obtained from sources considered reliable, but no representation is made as to its completeness, accuracy or timeliness. All information and opinions expressed are subject to change without notice. Information provided in this report is not intended to be, and should not be construed as, investment, legal or tax advice; and does not constitute an offer, or a solicitation of any offer, to buy or sell any security, investment or other product.