Market Update: June 15, 2026

Global markets navigated a volatile week as geopolitical tensions, resilient economic data, and shifting central bank expectations drove cross-asset performance.

U.S. equities declined (-2.55%), reversing earlier gains as escalation in the Iran conflict, renewed scrutiny on AI-related valuations, and policy changes around index inclusion weighed on sentiment. Weakness extended globally, with Europe modestly lower (-0.50%) and Asia mixed—Japan relatively stable while Korea saw sharper declines amid softening AI momentum.

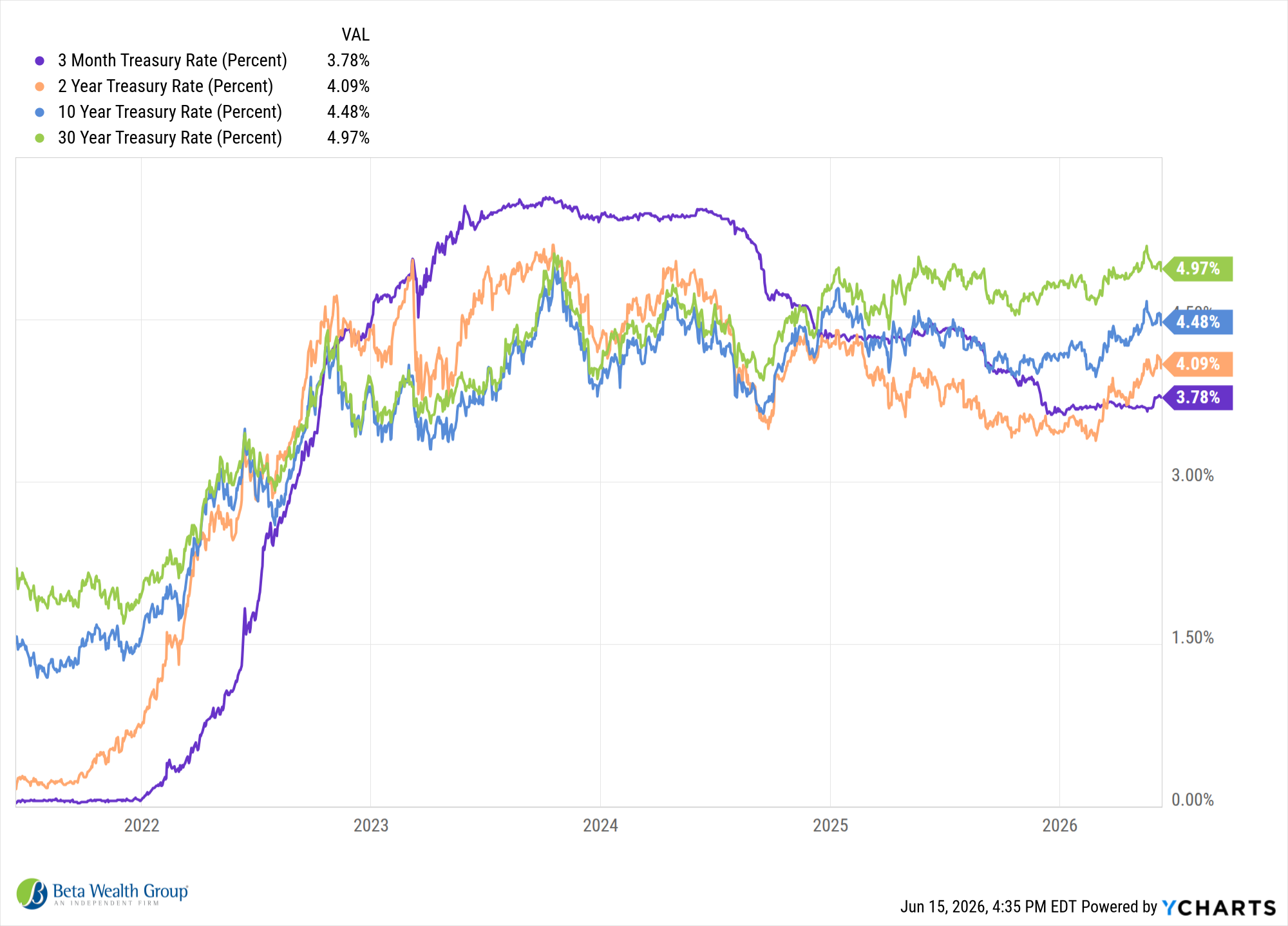

Fixed income markets reflected a “higher for longer” narrative. Strong U.S. labor data, including an upside surprise in nonfarm payrolls, pushed Treasury yields higher, with the 10-year closing at 4.53%. Globally, yields followed suit, as persistent inflation and resilient growth continue to constrain central banks’ ability to ease. The ECB’s recent rate hike reinforces this dynamic, even as growth in parts of Europe softens.

Commodities remain tightly linked to geopolitical developments. Oil prices pushed higher, with Brent near $93/barrel, driven by uncertainty surrounding Iran and potential supply disruptions in the Strait of Hormuz. Gold declined amid a stronger U.S. dollar and rising real yields, highlighting a shift toward more traditional “risk-off” dynamics.

From a macro perspective, the data paints a mixed but still constructive picture. U.S. activity indicators (ISM manufacturing and services) remain in expansion territory, while labor markets show resilience despite some softening in hiring rates. Abroad, Europe faces slowing growth alongside sticky inflation, while China’s momentum continues to stabilize at modest levels.

Looking ahead, markets will focus on central bank signaling, particularly the Fed under new leadership, and whether geopolitical risks or inflation pressures ultimately dictate the next move. For investors, this reinforces the importance of diversification and maintaining a disciplined approach amid evolving macro conditions.

The information above has been obtained from sources considered reliable, but no representation is made as to its completeness, accuracy or timeliness. All information and opinions expressed are subject to change without notice. Information provided in this report is not intended to be, and should not be construed as, investment, legal or tax advice; and does not constitute an offer, or a solicitation of any offer, to buy or sell any security, investment or other product.