Market Update: June 8, 2026

Last week offered a reminder that strong economic data can be a double-edged sword for markets.

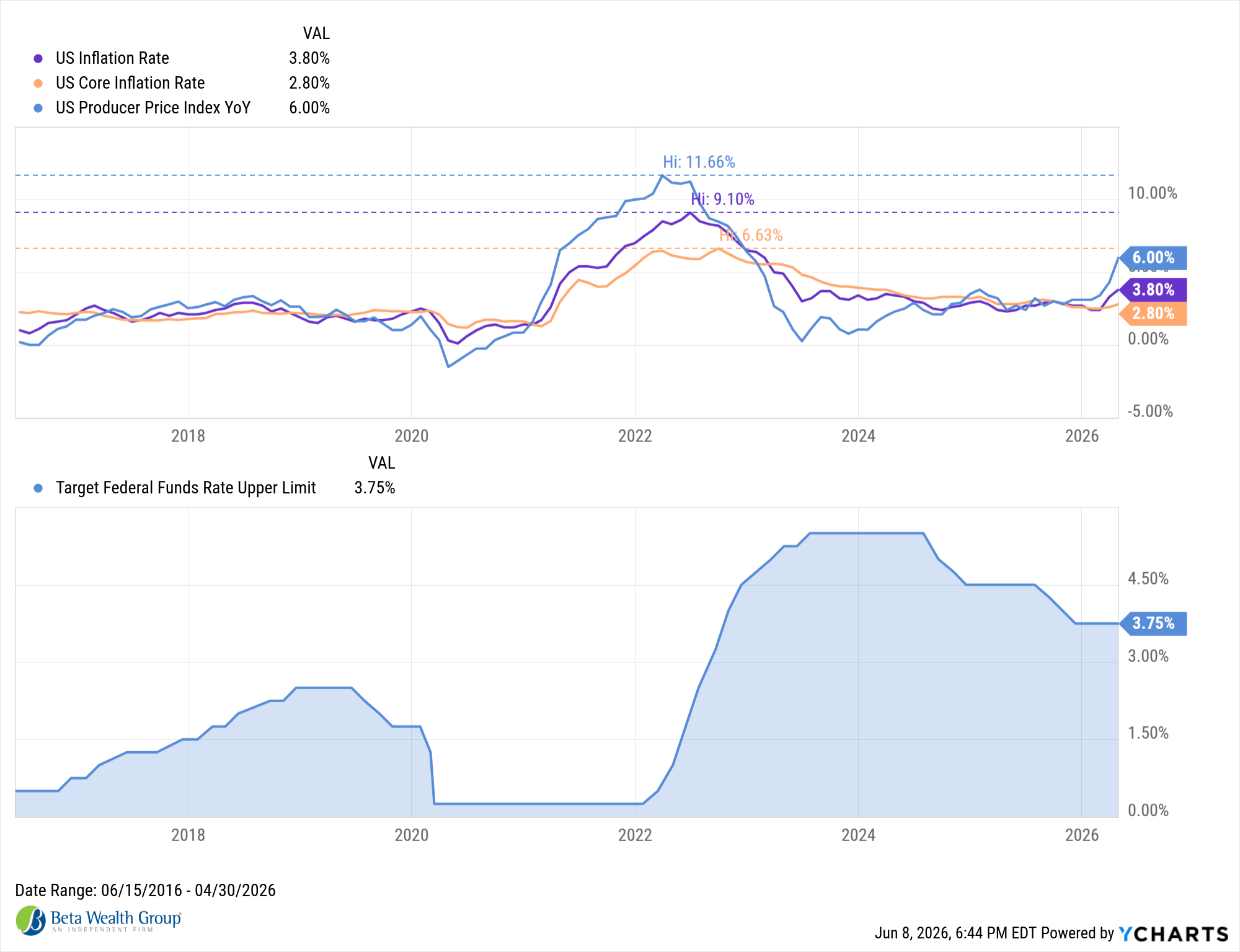

Recent releases pointed to resilience across the U.S. economy, including improved ISM manufacturing and services data alongside a solid May jobs report (172k payroll growth, unemployment steady at 4.3%). While supportive of growth, the data reinforced expectations that the Federal Reserve is unlikely to cut rates in the near term, prompting a shift in market sentiment.

Equities paused after a strong run, with major indices finishing lower for the first time in weeks. A notable mid-week rotation followed Broadcom’s earnings, where solid results but lackluster forward guidance triggered a sharp pullback in semiconductors. Leadership broadened briefly, lifting the Dow and Russell 2000 to highs, while prior leaders, technology, consumer discretionary, and communications, fell 4-6%. Energy and healthcare outperformed, each gaining over 2%.

Fixed income markets also adjusted, with yields moving higher across the curve. The 10-year Treasury broke above 4.5% and the 30-year surpassed 5.0%, weighing on both government and corporate bonds. A stronger U.S. dollar added pressure to international assets and precious metals.

Globally, developed markets held up better than emerging markets amid geopolitical tensions, Eurozone economic contraction (-0.3% Q1 GDP), and renewed trade concerns. Commodities were mixed: oil climbed above $90 per barrel on Middle East tensions, while gold, silver, and agricultural prices declined.

Looking ahead, inflation data will take center stage (U.S. CPI and PPI, global prints), with markets closely watching whether recent sector rotation evolves into broader participation or signals deeper pressure from higher rates and energy costs.

The information above has been obtained from sources considered reliable, but no representation is made as to its completeness, accuracy or timeliness. All information and opinions expressed are subject to change without notice. Information provided in this report is not intended to be, and should not be construed as, investment, legal or tax advice; and does not constitute an offer, or a solicitation of any offer, to buy or sell any security, investment or other product.