Market Update: March 24, 2026

Markets faced a volatile week as inflation concerns and geopolitical risks took center stage, pressuring both equities and fixed income. The Federal Reserve held rates steady as expected, but stronger-than-anticipated producer price data reinforced concerns that inflation may remain sticky, particularly as energy prices surge.

Global equities declined, with the S&P 500 down 1.56%, as escalating conflict in the Middle East drove oil price volatility and heightened uncertainty around growth. Energy infrastructure attacks and threats to key supply routes, including the Strait of Hormuz, pushed Brent crude sharply higher, while U.S. benchmarks remained relatively contained. Energy stocks benefited, rising roughly 3%, while more defensive sectors like utilities, materials, and consumer staples lagged amid shifting inflation expectations.

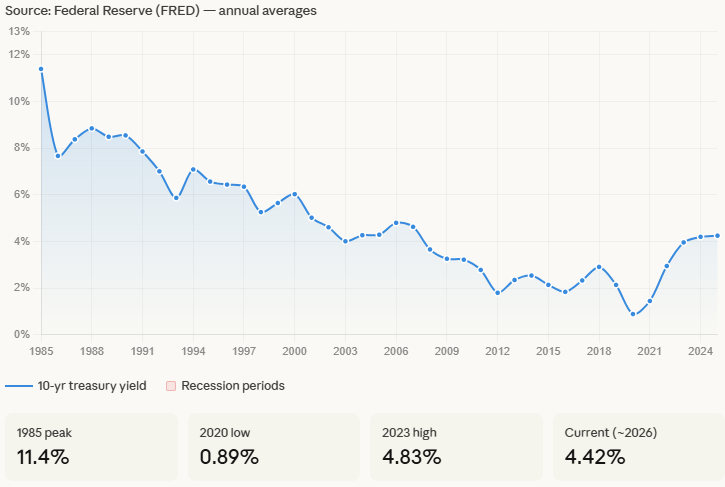

The bond market also repriced, with Treasury yields rising across the curve (2-year at 3.72%, 10-year at 4.28%) as investors adjusted to the risk of prolonged inflation and a more hawkish Fed. Notably, expectations for rate cuts have been pushed further out, reflecting the potential for sustained energy-driven price pressures.

Globally, central banks are increasingly cautious. The ECB and Bank of England held rates but signaled higher inflation projections, while policy divergence widened with Australia hiking and Brazil cutting rates. Meanwhile, the U.S. dollar strengthened on safe-haven demand.

The key market narrative remains the transmission from geopolitics to inflation and, ultimately, growth. Elevated oil prices not only risk prolonging inflation but could begin to weigh on economic activity if sustained. For investors, this environment reinforces the importance of monitoring energy markets closely, as they may dictate both monetary policy direction and broader market sentiment in the months ahead.

The information above has been obtained from sources considered reliable, but no representation is made as to its completeness, accuracy or timeliness. All information and opinions expressed are subject to change without notice. Information provided in this report is not intended to be, and should not be construed as, investment, legal or tax advice; and does not constitute an offer, or a solicitation of any offer, to buy or sell any security, investment or other product.