Market Update: May 4, 2026

Last week delivered a classic “growth with inflation pressure” backdrop for markets. The Federal Reserve kept policy rates unchanged, as expected, while U.S. Q1 GDP held near trend, durable goods improved, consumer sentiment stabilized, and manufacturing remained resilient. Housing was mixed, with price growth continuing to cool.

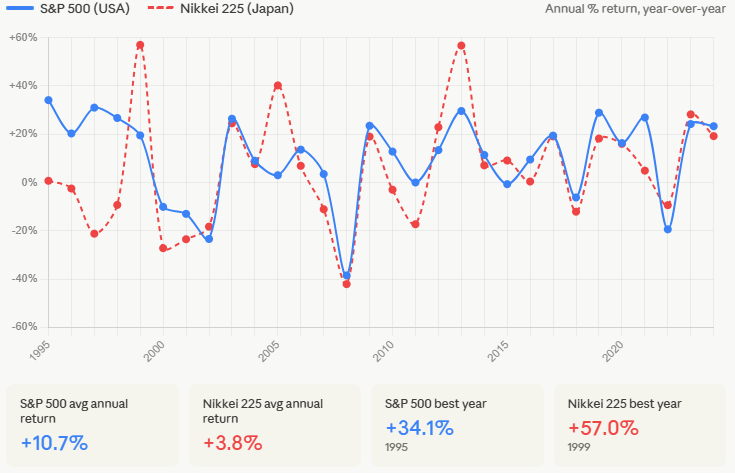

Equities finished broadly higher globally, led by the U.S. and Japan, while bonds softened as yields rose on renewed inflation concerns tied to oil. Commodities extended their gains, with energy once again driving performance as crude prices moved sharply higher.

In the U.S. it’s earnings, not geopolitics alone, that have become the main market driver. Several Magnificent 7 results helped shape sentiment, with Alphabet standing out and Meta facing pressure from heavier capex expectations. That dynamic underscores the market’s key debate right now: how much of today’s AI spending will ultimately translate into durable earnings power?

The earnings season backdrop remains constructive. By Friday, 63% of S&P 500 companies had reported, and among those, 84% beat EPS estimates and 81% topped revenue expectations. The blended Q1 earnings growth rate has climbed to 27.1%, led by technology, communications, and consumer discretionary.

Sector performance reflected the same pattern, with communications and energy leading the week while materials lagged. April was especially strong, with the S&P 500 rising 10% for its best monthly gain since late 2020, more than offsetting March’s decline.

Looking ahead, the next major test is the labor market, with Friday’s payroll report likely to shape expectations for the Fed’s path and the durability of the “higher for longer” narrative.

The information above has been obtained from sources considered reliable, but no representation is made as to its completeness, accuracy or timeliness. All information and opinions expressed are subject to change without notice. Information provided in this report is not intended to be, and should not be construed as, investment, legal or tax advice; and does not constitute an offer, or a solicitation of any offer, to buy or sell any security, investment or other product.